Are the Channel Islands still the place to go for non-UK London Stock Exchange listings? We explore the pros and cons – and how the changing landscape may or may not change the islands’ standing

Are the Channel Islands still the place to go for non-UK London Stock Exchange listings? We explore the pros and cons – and how the changing landscape may or may not change the islands’ standing

The Channel Islands have developed significant expertise for listing vehicles on capital markets, including the London Stock Exchange (LSE).

This capability has been built up over the past 20 years, with enthusiasm for capital-raising gathering pace from 2003/04 onwards.

It is true that activity dried up around 2007/08, when the financial sector went into meltdown, but it was a temporary blip as companies reassessed their position and investors licked their wounds.

The attraction of capital markets would build once again and, as the Channel Islands had already laid down a marker as the go-to place for such listings, the outlook looked good. But are the Channel Islands still jurisdictions of choice for non-UK LSE listings?

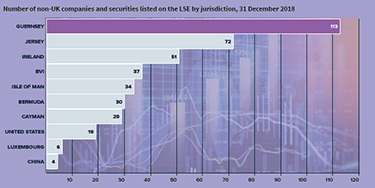

Ben Morgan, Partner and Head of the Corporate team in Carey Olsen’s Guernsey office, believes the islands – particularly Guernsey (see chart below) – will continue to maintain their dominant position for the foreseeable future.

Morgan points to several reasons for this strength – proximity to London; same time zone; well-established legal, accounting and banking expertise; similar company law to the UK; and a trusted regulatory regime.

Raulin Amy, a Partner in the Corporate team at Ogier’s Jersey office, agrees that these credentials are important and that the case in favour of the Channel Islands is strong – and continuing to build.

“Where a company may be targeting European investors on an IPO, there is certainly a preference for a Channel Islands-based company if an English company is not to be used,” he says.

“We are also seeing more Jersey companies being used to list elsewhere, particularly in New York, with Amcor and Clarivate being recent examples.

“In addition, we have certain European-based businesses – such as Glencore and Wizz Air – that are restructuring prior to IPO to insert a Jersey holding company at the top of the structure. So we know that using a Jersey company works from a European perspective.”

Having the edge

But couldn’t Ireland claim similar credentials to the islands, particularly in relation to its proximity to London and establishment as a financial centre?

Morgan believes the Channel Islands offer something different and have continued to build strong relationships with the City of London over the years – which has led to their taking the lion’s share of business.

“Unlike Ireland, Guernsey and Jersey are not in the EU. As Brexit rolls on, there will be concerns over the impact on market access. We are already outside the EU, so we know what our market access looks like. We are able to access LSE after Brexit, just the same way as before.”

He adds: “In terms of auditing, tax reporting and compliance specialists, the level of expertise in the Channel Islands is widely understood and has either been developed organically or brought in from the UK.”

Morgan insists that there is little difference between Jersey and Guernsey in terms of the quality of service and support they offer clients.

“When it comes to listing companies, London legal clients tend to recommend Guernsey,” he says. “Jersey does better than Guernsey in the establishment of non-investment companies – essentially holding companies.

“The way it’s worked out has been more by accident than by design – both islands offer similar advantages.”

Alex Adam, Partner, Advisory, at Deloitte in Guernsey, agrees that this is the way business has been shared between the two islands.

He is also keen to point out another key attraction of the Channel Islands. “In the past few years, the focus for many investors has been on income. Companies raising money via a Guernsey listing are able to distribute income back to investors much earlier.”

This is because boards in the Channel Islands can authorise a distribution on reasonable grounds that the company, immediately after the distribution, will satisfy the solvency test.

The same rule does not apply in the UK. Dividends can be made only out of ‘profits available for distribution’ as shown in the relevant accounts – which can take time to be recognised and delay distribution to investors.

According to Adam, this ‘income’ element has been a significant factor in recent years, which has contributed to a steady flow of income-producing investment companies listing via the Channel Islands.

“In general, Guernsey has, and continues to build on, its reputation for expertise in the alternative investment sphere. The more alternative the investment, the more Guernsey is seen as the place to go.”

The challenges

Are there any disadvantages to an LSE listing via the Channel Islands?

Raulin Amy at Ogier explains that for larger listings, where the company may wish to be included in the FTSE indices, there is a slight disadvantage as opposed to English companies.

The free float requirements are different and a larger percentage of the shares in the company will need to be in the hands of the public for a Channel Islands company.

However, the same applies for all other foreign companies looking to list – it’s just that there is a preferred regime for English companies applied by the FTSE committee.

The other challenges for Channel Islands companies, Amy adds, relate to the lack of international tax treaties, including bilateral investment treaties – which provide protection for companies that operate in the relevant foreign country.

While these are not major considerations for those looking to list on the islands, they may be part of the equation.

London connection

Understandably, much is made of the Channel Islands’ proximity to the City of London, as well as their longstanding, trusted relationship with the Square Mile.

But if London’s star is on the wane post-Brexit, where does that leave Jersey and Guernsey?

“A successful City of London is undoubtedly important for Guernsey and Jersey. If the City becomes less important, that has an impact on the Channel Islands,” Morgan warns.

“Anything can happen. Look at what’s occurred in Hong Kong. There could be a land grab from London, but I think most people would not bet against the City of London continuing to grow.

“There has been a gravitational pull of human capital from all over the EU to the City. There are a lot of talented people in London who don’t plan to leave. There has not been the drift back that some predicted and there’s unlikely to be one.”

If there is a threat to the Channel Islands from a changing landscape, Adam believes it is more likely to come directly from London itself – with the City taking business away from the islands.

“There is an argument that the UK will point to its own expertise and say: ‘We are not part of the EU now, so we can change our rules’ – and compete directly with the Channel Islands.”

Certainly, the Singapore-on-Thames idea has been put forward as a post-Brexit model for London – embracing East Asian laissez-faire, low tax, low spend and low regulation.

However, Adam believes that this is highly improbable, because the UK is more likely to want to maintain close alignment with the EU in support of market access.

As things stand, nobody knows how things will pan out regarding Brexit because the goalposts are being moved so frequently. Are we looking at worst-case scenarios or 11th-hour compromise?

Amy suggests that if the UK does thrash out a deal with the EU, this will only enhance the attractiveness of the Channel Islands to businesses and investors looking to access the capital markets via London.

It could also mean that Channel Islands companies will be considered as an option for more listings in the EU or elsewhere. Time will tell.